How much does it cost to start a trucking company? The honest answer is a range with a story inside it: roughly $25,000 to $150,000 or more for a one-truck operation with its own authority, depending mostly on one decision, whether you buy used equipment with cash or finance something newer. Registration, permits, and insurance down payments add $10,000 to $30,000 on top of the iron, and they arrive before you have hauled a single load.

Most guides on this topic hand you the same table of ranges and wish you luck. This one does something different: it walks through two real startups, line by line. Sammy Lloyd launched Lloyd Trucking in 2017 with about $25,000 all-in, truck, trailer, and authority, bought with cash. Rohit Handa launched Handa Transport in 2024 for about $150,000 all-in, financed. Here is every line item, what surprised both of them, and the number that actually decides whether a new trucking company survives its first year. Spoiler: it is not the price of the truck.

Start with the full bill. These are the real line items for launching a one-truck interstate operation with your own authority, with current published ranges:

Getting legal:

The iron:

Insurance (the shock line):

Add it up and the pattern is clear: the paperwork costs a few thousand dollars, the truck costs whatever you decide it costs, and insurance quietly rivals the trailer. A used-equipment cash launch can clear the whole list for $25,000 to $40,000. A financed newer-equipment launch runs $120,000 to $175,000 all-in, most of it debt.

Operating authority is your federal permission to haul freight for hire as your own company, issued by the FMCSA as an MC number. It is what separates an owner-operator with their own business from a driver leased onto someone else's authority. Everything in this article assumes your own authority; leasing onto a carrier skips most of these costs (and most of the upside). The registration itself is cheap at $300. What is expensive is being new: insurers and brokers both price the risk of a fresh MC number.

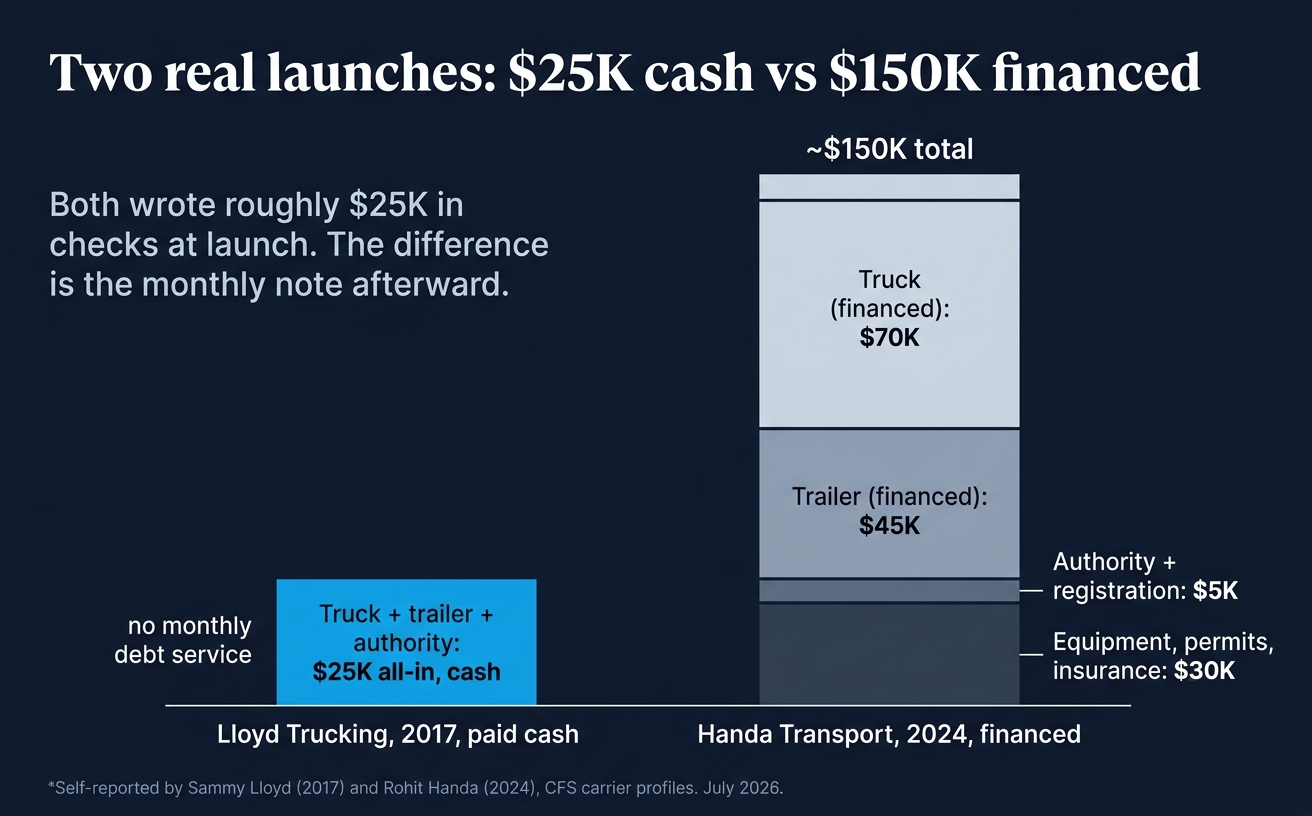

Ranges are abstract. Receipts are not. Here are two carriers we have profiled in depth, launched seven years apart with opposite strategies.

Lloyd Trucking, 2017: about $25,000, paid in cash. Sammy Lloyd spent months shopping with roughly $40,000 saved, looking for an older truck he could own outright. He bought a used Kenworth W900L, a trailer, and his authority for about $25,000 all-in, and kept the rest of his savings in reserve. His logic was blunt: "Not one day have I had $50,000 in my checking account... you don't need $50k to start." No truck payment meant every loaded mile fed the bank account instead of a lender, and an older paid-off truck meant repairs were annoyances, not emergencies stacked on top of a note (his full story).

Handa Transport, 2024: about $150,000, financed. Rohit Handa saved $60,000 over two-plus years as a company driver, banking $600 every week before he paid himself. At launch he financed a 2021 Freightliner Cascadia for $70,000 and a new dry van trailer for $45,000, spent about $5,000 on authority and registration, and with equipment, permits, and insurance called it "around $150,000 to start my own company... a really, really massive risk." Here is the detail that matters: of his $60,000 in savings, he deployed only about $25,000 and kept the rest as reserves, so that one bad month could not end the company (his full story).

Notice what just happened. Two carriers, seven years apart, opposite equipment strategies, and both wrote roughly $25,000 in checks to get started. One used it to buy the entire company; the other used it as the cash layer under a financed operation. The gap between a $25,000 startup and a $150,000 startup is not capability, both hauled the same freight in month one. The gap is monthly debt service, and who absorbs the damage when something breaks.

Neither path is "right." The 2017 cash path demands mechanical skill and tolerance for an older truck. The 2024 financed path buys reliability and warranty coverage at the price of fixed monthly obligations that do not care whether freight is slow. What both carriers shared was the part most new fleets skip: money left over after launch day.

Decide your equipment strategy by your wrench skills, not your ego. A $20,000 truck in the hands of an operator who can diagnose and fix it is a lower-risk startup than an $80,000 truck financed by someone who can't absorb the payment during a slow month. If you can't turn a wrench and can't yet afford newer equipment, the honest third option is driving for someone else another year and saving, which is exactly how both carriers in this article funded their launches.

Ask new owner-operators what surprised them most and the answer is rarely the truck. It is the insurance quote.

A brand-new authority has no loss history, no safety record, and statistically elevated odds of not surviving, so insurers price accordingly. Published guides put new-authority liability and cargo coverage at $15,000 to $25,000 per truck per year. The real numbers from our profiled carriers agree: Sammy Lloyd's new-authority premium ran about $14,000 a year (roughly $1,245 a month financed, against about $400 a month he had paid as a leased-on driver, a jump he called out specifically). Rohit Handa's first-year premium in 2024 was about $24,000 to $25,000.

Three things every new carrier should know about that number:

1. You do not pay it all at once, but you do pay to start it. Most new authorities finance the premium monthly after a down payment, typically $2,000 to $4,800, due before coverage binds. Budget the down payment as a launch cost and the monthly as a fixed cost.

2. It falls, meaningfully, if you keep your record clean. This is the part almost nobody tells you. After his first year with no tickets, no accidents, and no claims, Rohit's premium dropped from about $24,000 a year to $916 a month, roughly $11,000 a year, at renewal. A clean first year is not just safety, it is a five-figure raise in year two.

3. It scales with your choices. State of registration, truck age and value, cargo type, and radius all move the quote. Get real quotes from two or three trucking-specialty agents before you buy a truck, not after, because the premium can change which truck you can afford.

The other first-year price of being new is not a line item at all: some brokers decline fresh MC numbers outright, and the ones that take you may pay slower than you can afford to wait. That squeeze, and the tools for it, are covered in full in Freight Factoring for New Authorities.

Get insurance quotes before you commit to a truck. New carriers routinely budget for the truck first and discover the premium after, and a $24,000 first-year quote on top of an $80,000 truck note is how launches die in month two. The premium varies by truck value, state, cargo, and your record, so a real quote can change your equipment decision. And protect the record like an asset: one clean year cut a real carrier's premium by more than half at renewal.

Everything above gets you to your first load. What decides survival is the money that has to keep flowing after it.

Fixed monthly costs run whether you drive or not. Rohit's solo operation carries about $2,100 a month in fixed costs before fuel: insurance at $916, an ELD subscription, load board access, yard parking, and a maintenance set-aside of $800 a month. Sammy teaches the same discipline as cost per mile: his fixed costs on a newer-authority setup penciled to roughly 28 cents a mile, with fuel adding 31 to 44 cents depending on the truck's MPG. Know your version of these numbers before you quote your first rate, or you will haul loads that pay you to lose money.

The cash-flow gap is the killer. Brokers commonly pay 30 to 45 days after delivery. Fuel, insurance, and the truck note are due now. A new carrier can be profitable on paper and still die waiting for their own money, and this exact squeeze is why the failure rate for new authorities is brutal; Rohit cites the commonly repeated figure that 80 to 90 percent of new carriers do not make it, and points at debt plus slow-paying freight as the mechanism. The standard tools for the gap are broker quick pay and freight factoring, compared honestly in our quick pay vs. factoring breakdown and, for fresh authorities specifically, in Freight Factoring for New Authorities.

The reserve is the real startup cost. Both profiled carriers treated cash reserves as non-negotiable. Rohit saved $60,000 and deliberately spent less than half, keeping the rest so "my company does not fail." Sammy shopped for months below his budget for the same reason. A working formula: three to six months of your fixed costs plus one major repair (call it $10,000 to $20,000 for a one-truck operation) sitting in the business account on day one, untouched by the launch. If funding that reserve means a cheaper truck, buy the cheaper truck.

And the cautionary tale for year two: growth multiplies all of this. When Sammy added a second truck in 2023, bringing it online cost about $26,000 before it turned a wheel, and an engine rebuild later ran $35,000. The startup math in this article never really ends; it just adds trucks.

Undercapitalization, not equipment failure, is the leading way new trucking companies die. The pattern is always the same: every dollar goes into the launch, a broker pays in 40 days instead of 20, a repair lands in the same month, and there is no cushion. Whatever your startup number is, the operating reserve is part of it, not an optional extra. If you cannot fund three months of fixed costs on top of the launch, you are not underfunded by a little. You are one slow invoice from shutting down.

Can you start a trucking company with $10,000?

With your own authority, realistically no, not safely. Registration, formation, and permits consume $1,000 to $5,000, and a new-authority insurance down payment takes thousands more, before any truck exists. At $10,000 the honest paths are: keep saving (both carriers profiled here drove for someone else while they banked their startup fund), or lease onto an existing carrier, which trades independence for dramatically lower startup costs and cheaper insurance.

What is the cheapest way to start?

The 2017 Lloyd Trucking model: an older, mechanically sound truck bought outright, a used trailer, and your authority, roughly $25,000 to $40,000 all-in at current prices, plus reserves. The tradeoff is that the strategy assumes you can maintain an older truck. The cheapest path, as opposed to the cheapest launch, is often another year as a company driver saving aggressively: Rohit banked $600 a week for over two years to fund his start.

Should I buy or finance my first truck?

Cash for older equipment if you have the mechanical skills; financing only if your budget survives the payment during a bad month. The financed route buys newer equipment and fewer breakdowns, but it stacks a fixed note on top of insurance and fuel before revenue stabilizes. Whichever way you go, run the numbers with a real payment, a real insurance quote, and a real fuel estimate per mile. Our freight factoring calculator helps with the revenue side of that math.

How long until a new trucking company is profitable?

Published guidance says six to twelve months, but the variables are your debt load and your rate discipline. A cash launch with $2,000 in monthly fixed costs can be profitable in month one. A financed launch carrying $5,000+ in fixed costs needs consistent freight immediately, which is exactly what a fresh MC number makes hardest. This is why the first-year plan matters more than the launch: know your fixed costs, know your cost per mile, and know how you will bridge 30 to 45 day broker payment terms from day one.

Do I need my CDL before starting the company?

You need it before you can drive your own truck, and getting it first is the cheaper order of operations: $3,000 to $8,000 for training, then time as a company driver to bank startup savings and a safety record. Both carriers profiled here followed that sequence. Starting the company first and hiring a driver adds payroll to every number in this article and is a materially harder launch.

All figures here were verified as of July 2026 and change with the market: used truck prices move with freight cycles, insurance varies widely by state and record, and registration fees change by legislature. The two carrier startups are real, self-reported numbers from 2017 and 2024 launches, useful as anchors precisely because they are real, but your quotes are the numbers that matter. Build your budget from written quotes, not from any article's ranges, including ours.

"Not one day have I had $50,000 in my checking account... you don't need $50k to start."

New articles for owner-operators, delivered twice a month.